Court Quashes Administrative Subpoena Against AT&T

AT&T has filed unclaimed property reports at least as far back as 1999 in Delaware and in some states, back to 1993.

In the past 15 years, AT&T has escheated more than $400,000,000 in unclaimed property, including customer refunds, vendor checks, payroll, rebates, and credit balances, to the states, including Delaware.

In 2012, Delaware and other participating states began an audit, conducted by Kelmar, to determine the Company’s compliance with unclaimed property laws.

On December 6, 2019, AT&T sued Delaware over this unclaimed audit. In the Complaint, AT&T says, and asks the Court to declare, that

- Delaware impermissibly selected AT&T for audit;

- Using Kelmar, a self-interested party which the state has abdicated its power to, is unconstitutional;

- The audit requests violate the Fourth Amendment’s protections against unreasonable search and seizures;

- The unclaimed property estimation procedure is unconstitutional and preempted by federal common law;

- Moreover, that the retroactive application of the estimation procedure prior to 2017 is unconstitutional;

- The presumption of unclaimed property liability when a holder does not have records is void and unconstitutional;

- Delaware cannot apply the 2010 and 2017 amendments to an audit period beginning in 1992; and

- Delaware violated the Company’s due process rights when it kicked the Company out of the expedited audit program without any hearings.

Current Status of the AT&T Delaware Litigation

The AT&T v Delaware litigation kicked off with a complaint filed in the District Court for the District of Delaware. AT&T Capital Services Inc. v Geisenberger was filed on December 6, 2019. The case is 1:19-cv-022238.

Delaware filed a separate case in the state’s Chancery Court on December 9, 2019 to enforce the Administrative Subpoena. That case is State of Delaware, Department of Finance v. AT&T, Inc. CA No 2019-0985-JTL.

Delaware then filed a motion to dismiss in the federal court case on January 10, 2020 with AT&T filing opposition later in January. That motion is now pending before the Court.

Meanwhile, in the state action, the administrative subpoena was quashed on July 10, 2020.

AT&T Unclaimed Property Audit

On January 12, 2012, Delaware notified AT&T that it would be the subject of an unclaimed property audit. Kelmar, Delaware’s contingency fee auditor, was assigned the audit.

Other states participating in the audit include Florida, Illinois, Massachusetts, Michigan, New Hampshire, North Carolina, Pennsylvania, Rhode Island, and Tennessee.

Like other audits, the AT&T audit began with the normal document requests, which the Company responded to. In several instances, the Company notified Kelmar, and then Delaware, of concerns and objections over the scope and lack of particularity concerning the requests.

Significantly, Kelmar was able to complete its review of accounts receivable credits and found no liability.

While the audit was ongoing, Delaware amended its laws and permitted a one-time opportunity to enter into an expedited audit program. AT&T elected to proceed with the expedited audit program on December 7, 2017, with the intention of completing the audit within the two year time frame and under the belief that Delaware would be reasonable in its conduct during the expedited audit.

In an expedited audit, interest would be waived for holders that filed within the proscribed time period.

Delaware accepted AT&T into the expedited audit program on January 16, 2018.

Unclaimed Property History Note: The initial audit notice from Delaware was issued on January 12, 2012 and signed by Mark Udinski, then the State Escheator. He assigned the audit to Kelmar Associates. Mark Udinski retired from the State of Delaware in August 2013, and then promptly went to work for… you guessed it, Kelmar Associates.

Prior to retiring from the state and joining Kelmar, he issued more than 125 audit notices with the lion’s share going to Kelmar. At the time, the move created quite an uproar in the unclaimed property community.

For more information on the controversy, see Delaware Job Hop Stirs Flap by Vipal Mongal for the Wall Street Journal.

Disbursement Check Requests Burdensome and Unreasonable

During the expedited audit portion of the examination, Kelmar requested cumulative checks for 34 legal entities and 27 accounts for the time period June 1992 through March 2017, with detailed information concerning the payee name, address, amount, GL account, disposition, and more. This was for all states, not just Delaware. Seven months later, Kelmar added yet another account for which it demanded all the check information.

Side note: AT&T had three years prior provided information to Kelmar that 22 of these accounts were not disbursement accounts and did not disburse checks. Yet, Kelmar still requested the cumulative check information on these accounts. That is not a reasonable request.

AT&T estimates that the outstanding document request for the accounts seeks approximately 60 million transactions approaching $100 billion in value.

Then, Delaware required AT&T to prove that each check voided after 30 days was not in fact unclaimed property.

AT&T estimates that it will take 23.6 years to complete the research required on the checks.

In objecting to the completely unreasonable and burdensome request, AT&T proposed an alternative that would include data for 20 million payments and $30 billion in check value. Kelmar, predictably, denied the proposed alternative and doubled down on their request for all checks back to the year 1992.

AT&T has provided Kelmar with such information as check number, amount, date, address state, and disposition of the check, for over 10.5 million checks dating back to 2008 in 5 disbursing accounts. Due to privacy concerns for customers and vendors, AT&T did not reveal the payee name or full address.

Termination from the Expedited Audit Program

As one would expect following these burdensome, time consuming, and frankly unreasonable document requests, in late 2019, Delaware began sending letters to AT&T warning the Company that it was at risk of termination from the expedited audit program.

In a response to Delaware, AT&T reiterated that these requests were unreasonable and that Kelmar had provided no response to the objections. On October 28, 2019, Defendants again demanded that AT&T provide full disbursement records to Kelmar.

On October 31, 2019, Delaware terminated AT&T from the expedited audit program.

On November 8, 2019, Delaware issued a subpoena, purportedly under authority from the February 2017 amendments. The subpoena demands the same unreasonable and burdensome requests for the disbursement checks discussed above, as well as additional rebate requests that were also outstanding and similarly burdensome. The demand for personal appearance by a company representative with complete documents was for December 9, 2019.

AT&T is now fighting this subpoena under Fourth Amendment unreasonable search and seizure and Fourteenth Amendment due process grounds.

Delaware Did Not Have A Record Retention Requirement Prior to 2017

Delaware amended its laws in 2017 to remedy many of the problems identified in the Temple Inland case. Two of those changes were to require companies to retain records necessary to complete an audit and when those records are not available, to allow the state to make an estimation of the company’s liability.

Prior to these amendments, Delaware had no statutory record retention requirement. Since companies were not on statutory notice, they maintained records in accordance with common tax record retention policies – 7 years. For various reasons, some companies may have extended that to 10 years. No company would maintain full and complete and auditable records for nearly three decades.

Delaware, and its contingent fee auditor Kelmar, was relying on the fact that companies would not have records for the entire look-back period of an audit.

Did I mention that prior to 2017, the Delaware statute did not provide for a look-back period? It wasn’t until the 2017 amendments that the Delaware unclaimed property law specifically provided for a 10 year look-back period.

Legal Claims in AT&T v Geisenberger

Flawed Estimation Methods Lead to Significantly Misleading Results

AT&T seeks a declaration that Delaware may not retroactively apply their estimation methodologies when a holder does not maintain adequate records prior to the law’s amendment requiring that a company maintain such records. AT&T argues that the estimation method that is codified in the Delaware statute is not based on actual holder records and “leads to significantly misleading results.”

Like prior cases concerning the audit methodology, AT&T says that using checks issued to payees located in states other than Delaware is unreasonable because even if the property in unclaimed, it is not reportable to Delaware.

To further use this data in the process of an estimation is a violation of substantive due process rights because it will once again subject the holder to multiple liabilities for the same property, as other states could claim the property and/or complete its own estimation. In fact, multiple liabilities is a foregone conclusion and unavoidable since the estimation methodology relies partly on prior unclaimed property reports filed with other states

Using the unclaimed property in recent years that is or was reportable to other states has already been determined to produce “significantly misleading results” in Temple-Inland. This estimation method “is all an absolute fiction designed to maximize the revenue stream to the state and Kelmar’s coffers. Defendants treat the entire amount of estimated liability as owner-unknown property, which they then escheat according to the secondary rule enunciated in Texas v. New Jersey and Delaware v. New York.”

The same method used in Temple-Inland was eventually included in the October 2017 regulations made pursuant to the February 2017 statutory amendments.

Getting into the nuts and bolts of the audit and estimation procedure, AT&T also seeks to declaration that the presumption of abandonment for checks voided after 30 days, along with a lack of record retention provisions prior to 2017, violates both the Takings and Due Process Clauses of the Fourteenth Amendment and the Ex Post Facto Clause of the US Constitution.

Void for Vagueness

AT&T also argues that the statutory requirement that permits the State to “use a reasonable method of estimation” are so vague that it violates the Company’s due process rights.

In it’s Complaint, AT&T says:

The power to define a vague law is effectively left to those who enforce it, and, as set forth herein, private auditors who enforce the DUPL operate without court oversight in a setting of unconstitutional secrecy and informality. The vagueness of the DUPL — coupled with its absence of any standards to apply and enforce the law — facilitates prejudiced, arbitrary, discriminatory and overreaching exercises of state authority by Delaware’s delegates. Delaware’s delegation of authority is so extensive that is has led to arbitrary and overreaching assessments of liability for unclaimed property, such as in the case of Temple-Inland.

In effect, AT&T says that the estimation methodology is not spelled out appropriately in the laws or regulations and such that it has been, it was Kelmar that dictated that policy. Delaware using Kelmar’s methodology and not Kelmar using Delaware’s methodology is just another example of Delaware abdicating its power to this private contractor. And by abdicating its power, Delaware has allowed for an unconstitutional process to continue and flourish, harming companies that call the state home.

Unconstitutional Taking of Private Property

The estimation process is also an unconstitutional taking of private property for public use without compensation, since the estimation is a transfer of AT&T’s private property rather than a transfer of another’s private property that would then be held in trust by the state.

The amounts collected under unclaimed property compliance and audits is deposited in to the Delaware General Fund. That is a very clear intent of public use of the funds collected.

Limits on Delaware Subpoena Power

After Delaware terminated the expedited audit, the state issued a subpoena for records from 1992 to 2010.

AT&T argues that Delaware does not have the power to subpoena records prior to February 2, 2017, when the statute was amended to include a subpoena power.

Requiring the production of records, records that cannot lead to a constitutional estimation result, is unreasonable and burdensome.

The Delaware action in the state’s Chancery Court, filed on the Monday after the AT&T lawsuit filed in federal court, is to enforce the administrative subpoena.

In July 2020, the Chancery Court quashed the subpoena as being an abuse of the court’s process. More on that in a minute.

Deprivation of Due Process Rights by Terminating Expedited Audit

AT&T alleges that Delaware has deprived AT&T of due process and to be free of unreasonable searches and seizures and significantly harmed the Company by terminating its participation in the expedited audit process.

When Delaware terminated the Company’s participation, it did so without any pre or post deprivation hearing. The decision, made by the State Escheator, subject to review by only the Secretary of Finance.

There was no administrative hearing where the Company could make arguments that it should remain in the program. AT&T says that at no time has the company has an opportunity to defend itself in the removal from the expedited audit process.

Remember, the expedited audit process would waive interest from any late reported property, including any estimations. In a regular audit, there is a mandatory assessment of interest and penalties. By terminating the expedited audit process, AT&T becomes harmed by this mandatory assessment for asserting its Fourth Amendment rights.

Attacking Kelmar as the Auditor

While many holders have long complained about Kelmar and other third party contingent fee auditors, AT&T is going on the offensive, saying that Delaware’s use of Kelmar is a violation of the Constitution.

Are Unclaimed Property Audit Workpapers Subject to FOIA Requests?

Specifically, AT&T says that since Kelmar represents multiple states in the same audit, Kelmar violates AT&Ts due process rights because it exposes confidential and proprietary records to public inspection due to conflicting laws in different state unclaimed property laws.

I have often said that the only thing that I can’t see in an unclaimed property audit is the secret formula that Coke uses to make Coca-Cola.

And it is one thing for the state to look at those records in an audit. But what if all the audit workpapers, including customer names, employee and vendor contracts, and every. single. financial. transaction. was made available to your competitors because of an audit? Could audit workpapers be subject to a FOIA?

The public records laws of both Illinois and Massachusetts, two states participating in the audit, could make any information received by a government contractor (Kelmar) in performance of a government function (unclaimed property audit) public records that must be disclosed in connection to a valid FOIA request.

Delaware assigning Kelmar to work on a multi-state audit with Illinois and Massachusetts participating could conceivably open up the AT&T financial records to FOIA requests through Illinois or Massachusetts.

AT&T says that Delaware forcing these records, which will not be kept confidential, to be turned over to Kelmar, is a violation of due process rights and an illegal search.

Contingent Fee Arrangements

AT&T also says that the contingent fee arrangement with Kelmar violates AT&T’s rights because Kelmar becomes a real party in interest that performs all legally significant audit tasks and assessments, resulting in AT&T submitting a dispute to a self-interested party.

AT&T, and most other holders will agree with, says that Kelmar is the party conducting the audit, issuing information requests and recommendations to the states which then rubber-stamp the results.

This behavior by Kelmar and the states is a violation of the holder’s rights since the rubber stamp offers no meaningful opportunity to challenge the decisions made by Kelmar. As can be seen in this audit of AT&T, all objections were ignored and even the responses to the objections made directly to the state were often responded to by Kelmar.

Since 2014, Delaware has paid Kelmar at least $156,040,477.14 for unclaimed property auditing services.

New Kelmar Contract

In Delaware’s motion to dismiss filed January 10, 2020, Delaware provided a brand new contract between the state and Kelmar (PDF, opens in new window).

Notice, that this contract is dated December 31, 2019, after the initial lawsuit was filed in federal court by AT&T and also after Delaware’s lawsuit in Chancery Court to enforce the subpoena.

In this contract, there are three main services that Kelmar is to provide – general ledger audits at an hourly rate, securities exams on a contingency, and other services, which are the back-office functionality that Kelmar provides to the state, at an hourly rate. There are also volume discounts once invoices hit certain thresholds of $7.5 million and $11 million, just to give you an idea of the type of fees that the state and the company expect to bring in.

While this new contract presumably details an hourly rate for general ledger examinations, it does have quite a few issues for unclaimed property holders.

For example, the Kelmar contract specifically says that if another state, under the first priority, exempts property or has a deduction or other exclusion, then Delaware can claim the property as the state of incorporation, under the second priority rule.

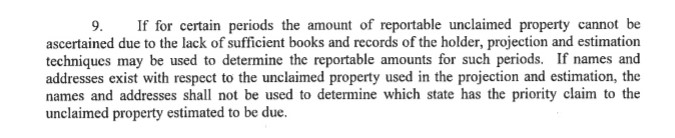

Meanwhile, another section specifically says that when “names and addresses exist with respect to the unclaimed property used in the projection and estimation, the names and addresses shall not be used to determine which state has the priority claim to the unclaimed property estimated to be due.” (emphasis added)

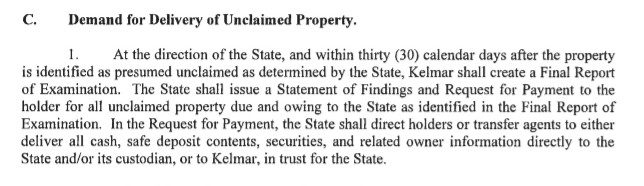

Then there is this provision, that seems to remove all authority from the State and hand it all to Kelmar for the final report and demand for payment. Kelmar shall create a Final Report of Examination. The State shall issue a Statement of Findings and Request for Payment to the holder . . . as identified in the Final Report of Examination. In the Request for Payment, the State shall direct holders … to deliver [payment] directly to the State and/or its custodian, or to Kelmar, in trust for the State. (emphasis added)

As an unclaimed property attorney, I am not sure that including this contract in the motion does what the state hopes it does. It may address the point that Kelmar is now getting paid by another payment arrangement than what was previously, and at the time of the complaint, being used.

The contract does, however, highlight several of the other issues that AT&T complained about in their initial filing, including state decision making and unlawful delegation of authority; use records not likely to lead to reportable property; an estimation procedure that leads to artificially high audit liabilities; and the disregard of sovereign state positions (and several federal court decisions) on the first priority rule.

Selection of AT&T as an Audit Target

One of the complaints that AT&T has of the entire audit is that AT&T was selected for an audit based on its perceived profitability as an auditee and not based on any neutral criteria or criteria bearing a rational relationship to legitimate governmental interest.

If the auditor is recommending audit targets, which are then rubber stamped by the states, it is in their best interests to select audit targets and use such procedures (estimations) that will result in the largest potential assessments so that their contingency fee will be maximized.

Even the recent statutory amendments and regulations promulgated pursuant to the amendments, the procedures that were enacted by Delaware “conveniently” mirror the procedures that Kelmar had used for years.

Delaware’s Motion to Dismiss

The main argument that Delaware makes in their motion to dismiss is that the federal court should allow the after filed state court case to proceed, as a matter of comity. If the Court does decide to hear the case, Delaware asks it to dismiss many of the counts because they are not yet ripe, as a matter of law.

Delaware wants a Delaware state court, not the federal court, to decide issues of state law, notably the enforcement of the subpoena. Notably, however, the Chancery Court action only asks the Court to enforce the Subpoena and require AT&T to produce documents pursuant thereto. It does not address any of the other issues raised in the AT&T federal court complaint.

In the Univar case last year, a federal court judge did say that several of the claims were not yet ripe because the company had not yet been subjected to an audit. However, the judge did permit the case to continue on due process and equal protection claims. That case though was put on hold to allow the state court to decide on the application of the subpoena.

Remember, the AT&T case is distinctly different than the Univar case. Here, AT&T was dismissed from Delaware’s expedited audit program, which has its own benefits for participation. That alone should be sufficient to make the case ripe, as an injury has actually been sustained by the Company.

Other than a few argumentative slights, Delaware didn’t have anything substantial to add to the commentary on how the audit proceeded. They did throw in a “filed this action challenging the constitutionality of the Escheats Law, calling into question whether the Company had ever intended to comply with the Subpoena and whether it had been negotiating in good faith.” Of course, the State failed to mention just how burdensome said requests were to AT&T.

Court of Chancery Quashes Administrative Subpoena

Earlier, I noted that Delaware had filed suit in the state’s Court of Chancery to enforce the administrative subpoena.

However, on July 10, 2020, the Court of Chancery said that AT&T “has met its burden to show that the scope of the subpoena is so expansive that enforcement would constitute an abuse.” (emphasis added)

While the statute of limitations is not a bar to the state’s investigation,

If it appears highly unlikely, even impossible, that the State Escheator could reach property from a given year, then it becomes more likely, all else equal, that the subpoena is improper. The extent to which an information request goes beyond the statute of limitations thus becomes part of the inquiry into whether it would represent an abuse of the court’s process to enforce a subpoena, absent some creditable explanation addressing how the information would be used.

Meanwhile, the state’s request for all checks, even those with addresses outside Delaware which it would not be able to claim under the Escheat Law,

All else equal, however, a broad request for information concerning property that does not fall into any escheatable category makes it more likely that enforcing a subpoena would be an abuse of this court’s process.

When it comes to the volume of requests, an “all checks issued” request is broad. While it is authorized by the Escheat Law,

the expansive nature of the request will be taken into account when evaluating whether enforcing the Subpoena would be an abuse of this court’s process.

In summary, the Court’s words say it best:

Here, a combination of factors supports a finding that to enforce the Subpoena would be an abuse of this court’s process. The Subpoena is expansive, both as to the time period it covers and the subject matter is embraces. Temporally, the Department requests records of rebates and checks going back to 1992. The Department did not provide any rationale for seeking information going back so far. The period covered extends sixteen years beyond the point at which the Old Statute of Limitations would prevent the State Escheator from recovering unclaimed property. The Department did not offer any reason why the Old Statute of Limitations would have been displaced by the New Statute of Limitations, choosing merely to assert in ipse dixit fashion that the New Statute of Limitations applied. Even if it did, the request extends five years beyond the point at which the New Statute of Limitations would prevent the State Escheator from recovering unclaimed property. The Department seems to be pursuing information about property that it knows it cannot recover, and it has supported those requests with only bareboned allegations.

Similar problems infect the subject matter of the Subpoena. Covering the full temporal period, the Department asks for records regardless of whether the last-known address as reflected on AT&T’s records was located in Delaware. Under Nellius and Texas v. New Jersey, records with last-known addresses outside of Delaware are almost certainly non-escheatable. Once again, the Department seems to be pursuing information about property that it knows it cannot recover, and it failed to support those requests with any creditable explanation.

Also covering the full temporal period, the Department asks for records of all checks, regardless of whether they have been marked cashed, cleared, voided, stopped, reissued, or still outstanding. This is a massive request for information, and one would expect the Department to have articulated some rational basis for seeking it. As discussed previously, it is of course true that an agency need not provide a reason for seeking information, but when an agency makes so broad a request, it should anticipate having to proffer some justification.It seems evident that the Subpoena will sweep in a vast amount of irrelevant data….

The Department thus sees even irrelevant documents as relevant to “the audit” and “the audit process.” That rationale has no limiting principle. (Internal citations omitted)

The judge continued on, detailing why there are additional concerns, including how Delaware delegates its investigation to Kelmar, the third-party auditor, to use the state’s investigatory authority “to Kelmar to use as it sees fit.”

Since Kelmar is compensated on a contingent basis, the company has an “incentive to engage in aggressive enforcement tactics. It potentially creates a pernicious incentive for Kelmar to serve broad information requests and engage in expansive audits that impose substantial burdens on companies, thereby inducing settlements that generate income for Kelmar. The breadth of the Subpoena in this case is suggestive of such tactics.”

Meanwhile, the judge notes that Kelmar has incentive to gain such information for its own use – as the company represents other states. It is not just Delaware property that it seeks to claim, but all the other states that the auditor represents. While that would be helpful for Kelmar and the other states, Delaware’s Escheat Law is not there to help the other states.

Because Delaware failed to provide guidance on how it could modify the subpoena, the court instead quashed the subpoena in its entirety. However, the court did indicate that the state could appeal the decision or craft a new subpoena.

What’s Next?

There are some loose ends that must be tied up, including a final order to implement the judge’s ruling to quash the subpoena. Delaware can then choose whether to craft a new subpoena that would be more limited in scope or it can appeal the decision.

The federal action remains outstanding. In January, Delaware filed a motion to dismiss which AT&T opposed.

What Should Holder’s Do Now?

Holders should continue to comply with annual compliance requirements, as no matter the outcome of this lawsuit, a good compliance program is always your best defense to an audit. In fact, much of the outcome in quashing the subpoena related to the statute of limitations that applied because AT&T has filed unclaimed property reports.

As a reminder, the next Delaware unclaimed property reports are due March 1, 2021.

If you are currently in an audit or Delaware Voluntary Disclosure Agreement, a process that uses substantively the same estimation process, you should monitor any developments in this case. While the subpoena may be quashed, this case isn’t over. The state will presumably attempt to continue by crafting a more narrow subpoena, limited in particular to the years in scope.

To receive updates, you may subscribe to the DeCarrera Law Unclaimed Property Newsletter where significant updates will be discussed.

Return to Unclaimed Property Litigation